CREA Updates Resale Housing Market Forecast

Ottawa, ON March 15, 2022 – The Canadian Real Estate Association (CREA) has updated its forecast for home sales activity via the Multiple Listing Service® (MLS®) Systems of Canadian real estate boards and associations in 2022 and extended the forecast into 2023.

Home sales have kicked off 2022 below 2021 levels, while price growth has continued to set records. This is consistent with strong demand meeting end-of-month inventory levels that are lower than they have ever been.

Along with the ongoing supply crisis, the other main factor expected to impact housing markets this year and next will be higher interest rates.

While discounted five-year mortgage rates have already begun to rise – a jump last spring followed by a steady upward trend since last October – and are now back above pre-COVID-19 levels, the Bank of Canada has only just announced its first quarter point hike in early March.

Analysts surveyed by Bloomberg Economics see the overnight rate ranging from 1.75% to 2.75% by the end of 2023. That said, given markets are currently pricing in 1.75% by the end of 2022, it is more likely to be the latter. That would make for nine Bank of Canada quarter-point rate hikes by the end of next year.

Having said that, it’s important to note Canadian borrowers must qualify for their mortgage loans at the stress test rate (currently set at 5.25%), which is currently somewhere in the range of 245 basis points above the typical discounted five-year rate.

The original intent of the stress test was a buffer of around 200 basis points, which is likely why the Office of the Superintendent of Financial Institutions (OSFI) chose not to move the stress test rate following their December 2021 re-evaluation.

As such, recent higher market rates have not really made it any more difficult to qualify for a mortgage, and borrowers are still being stress tested at a very robust level.

Another wildcard are the housing policy changes announced in last year’s federal election campaign. Which of these will become policy in 2022 and beyond and how will these affect housing markets across Canada? The answers should become clearer when the Federal Budget is published later this spring.

Finally, to quote the Bank of Canada from their most recent policy announcement: “The unprovoked invasion of Ukraine by Russia is a major new source of uncertainty. Prices for oil and other commodities have risen sharply. This will add to inflation around the world, and negative impacts on confidence and new supply disruptions could weigh on global growth. Financial market volatility has increased. The situation remains fluid and we are following events closely.”

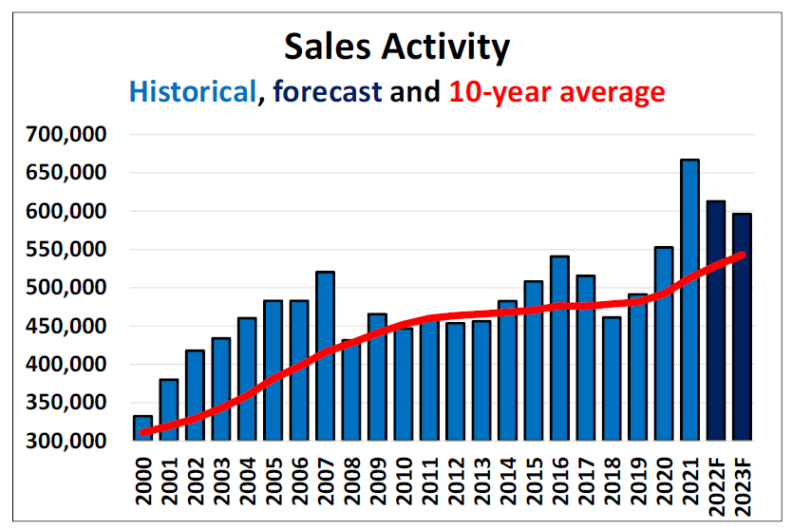

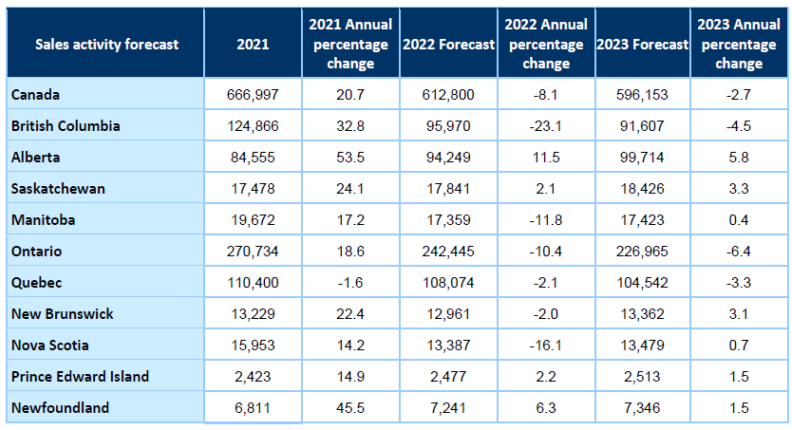

With all of that said, some 612,800 properties are forecast to trade hands via Canadian MLS® Systems in 2022 — a decline of 8.1% from 2021 but still the second-highest annual figure ever by a sizeable margin.

This projection is basically the same as it was in the December 2021 forecast, though under the surface, downward revisions to British Columbia, Manitoba, Ontario, Quebec, New Brunswick and Nova Scotia offset a considerable upward revision to the sales forecast for Alberta, along with smaller upward revisions to Saskatchewan and Newfoundland & Labrador.

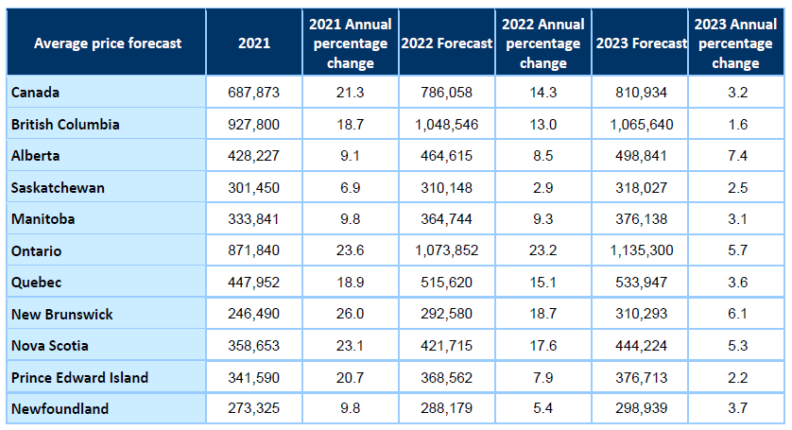

The national average home price is now forecast to rise by 14.3% on an annual basis to $786,000 in 2022. Not surprisingly, this is higher than the previous forecast, as prices have continued to set new records, reflecting the unprecedented imbalance of housing supply and demand. The number of months of inventory nationally was a record-low 1.6 in December 2021, and January and February 2022. The long-term average for that measure is a little over 5 months. It is quite possible the risk to this price forecast is still to the upside.

Home sales are forecast to remain historically strong in 2023 while continuing to move slowly back in the direction of the longer-term trend. Limited supply, higher prices and higher interest rates are expected to further tap the brakes on activity and price growth in 2023 compared to 2022, particularly in Canada’s most expensive markets.

National home sales are forecast to edge back a further 2.7% to 596,150 units in 2023 – still the third-best year on record. This easing trend is expected to play out most notably in British Columbia, Ontario and Quebec. Alberta and Saskatchewan are forecast to buck the trend with moderate sales gains in 2023.

Other provinces are forecast to see fairly little change in sales between 2022 and 2023 as economic growth, population growth, and supportive demographic trends under the surface are counterbalanced by supply and affordability challenges.

The national average home price is forecast to rise by a modest 3.2% on an annual basis to just under $811,000 in 2023. While the $800,000 mark may seem an unlikely milestone to hit given where the market was just a couple of years ago, it should be noted that with the national average price having already surged (though likely only temporarily) to more than $816,000 in February 2022, this is a conservative forecast.

The Quarterly Forecast data is available to download in Excel (.xlsx) format.

Legal

Copyright

All materials, content and data (collectively, “Content”) on this site are copyrighted and are owned either by The Canadian Real Estate Association (CREA) or the real estate board or other third party that has supplied the Content to CREA. This website, and all Content available on this website, is owned by, or licensed to, CREA.

Except as expressly provided for in Section 2, Content available on this site is intended for private, non-commercial use by individuals. Any commercial use of the Content in whole or in part, directly or indirectly, is specifically forbidden except with the prior written authority of CREA.

Users may, subject to these Terms of Use, print or otherwise save individual pages for private use. Except as provided for in Section 2, Content may not be modified or altered in any respect, merged with other data or published in any form, in whole or in part. By accessing this site, or by downloading Content, the user confirms agreement with, and acceptance of these Terms of Use.

MLS® HPI Data and News Release Content

This website makes MLS® HPI data available for download at https://www.crea.ca/housing-market-stats/mls-home-price-index/hpi-tool and news release information for download at https://creastats.crea.ca/en-CA. and https://www.crea.ca/housing-market-stats/quarterly-forecasts.

The user may, subject to these Terms of Use, download this Content for general reference by the user in order to conduct analyses, to generate graphs and charts, and in the reporting of results, conclusions, and forecasts. This Content must not be published or displayed in whole or in part in any such analyses, graphs, charts, results, conclusions or forecasts without the prior written consent of CREA. CREA must be attributed as the source of the Content in any and all displays. The user shall not use the Content or any results, graphs, charts or otherwise derived from the Content, for the purposes of resale or commercial distribution.

Trademarks

Not all real estate agents are REALTORS®.

REALTOR®, REALTORS® and the REALTOR® logo are certification marks owned by REALTOR® Canada Inc., a corporation jointly owned by the National Association of REALTORS® and CREA. The REALTOR® trademarks are used to identify real estate services provided by brokers and salespersons who are members of CREA and who accept and respect a strict Code of Ethics, and are required to meet consistent professional standards of business practice which is the consumer’s assurance of integrity.

MLS®, Multiple Listing Service®, and the associated logos are all registered certification marks owned by CREA and are used to identify real estate services provided by brokers and salespersons who are members of CREA.

Other trademarks may be owned by real estate Boards and other third parties. Nothing contained on this site gives any user the right or license to use any trademark displayed on this site without the express permission of the owner.

Links to Website

Users may link to the website. However, CREA reserves the right to refuse a link at any time at CREA’s sole discretion. The user agrees to remove any link to the website at CREA’s request.

Links to Third Party Sites

This website may contain hyperlinks to websites operated by parties other than CREA. Such hyperlinks are provided for the user’s reference only. CREA does not control such websites and is not responsible for their contents or the privacy or other practices of such websites.

Privacy

The user acknowledges that their personal information will be used by the website in accordance with the website privacy policy located at https://www.crea.ca/privacy/.

Not Professional Advice

The Content on this website, including but not limited to articles and podcasts, are for information purposes only and are not a substitute for professional advice. Users who need professional advice should consult a lawyer or other qualified professional.

Passwords

Some sections of the website may be password protected. Only those persons who have been validly issued passwords by CREA are authorized to access the website. The user agrees to provide CREA with accurate, complete, and updated registration information. Failure to do shall constitute a breach of these Terms of Use, which may result in immediate termination of the user’s access to the website. Furthermore, the user warrants that he/she will not:

- Divulge, share or compromise his/her password, or use any other user’s password.

- Enable or permit other persons to access the website.

- Make unauthorized copies of any information on or displayed through the website.

- Take any action which might reasonably be construed as injurious or detrimental to the interests of any other users or to CREA.

- Permit unauthorized persons access to the website.

Messages

The website may allow users to send messages to other persons or post content that is visible to many users simultaneously (collectively, “Messages”). The user agrees not to use the website to harass or abuse, send spam or other unwanted communications, or send unlawful, libelous, obscene, discriminatory or otherwise objectionable Messages including Messages that:

- infringe, misappropriate or violate any intellectual property or other rights of any third-party;

- are defamatory, harmful to minors, obscene or child pornographic;

- contain any viruses or programming routines intended to damage the services or any software, hardware or other technology used to provide the services or surreptitiously intercept or expropriate any data or information; or

- are false, misleading or inaccurate.

CREA is under no obligation to review the content of Messages sent through the website but may do so at any time in order to comply with any law, government request, or in the interest of operating the website. CREA may remove or block any Message for any reason.

Liability and Warranty Disclaimer

CREA makes no representations about the suitability of the Content published on or through this website. Everything on this website, including but not limited to all Content, is provided “As Is” without warranty of any kind including all implied warranties and conditions of merchantability, fitness for a particular purpose, title and non-infringement. Neither CREA nor any of its suppliers shall be liable for any direct, incidental, consequential, indirect or punitive damages arising out of the user’s access to or use of this website or the Content.

Disruption of Service

CREA may suspend, discontinue or change any aspect of the website or Content without notice or liability.

Indemnification

The user agrees to indemnify and hold CREA harmless from any and all liability, damages or expenses, whatsoever due, arising from, directly or indirectly, any cause of action arising out of their use of the website or the Content, including from any Messages sent through the website.

Updates, Upgrades, and Revisions

CREA may at any time revise these Terms of Use by updating this posting. All users of this site are bound by these conditions and should therefore periodically visit this page to review any changes to these requirements. The user’s continued use of this website or the Content following the posting of any changes constitutes acceptance by the user of such modifications.

No Waiver

CREA’s failure or delay to enforce any of the terms and conditions under these Terms of Use shall not operate as a waiver of any of CREA’s rights or privileges under these Terms of Use.

Language

If these Terms of Use are translated into a language other than English and there are conflicts between the translations, the English version shall prevail and control.

Governing Law

These Terms of Use shall be governed by the laws of Ontario, Canada. The courts in Ottawa, Ontario, will have exclusive jurisdiction to hear and decide any disputes relating to these Terms of Use.

Contact Us

If you have any comments or questions, please contact:

THE CANADIAN REAL ESTATE ASSOCIATION

200 Catherine Street, 6th Floor

Ottawa, ON

K2P 2K9

Tel: 1-800-842-2732

(613) 237-7111

Email: info@crea.ca

- 30 -

About the Canadian Real Estate Association

The Canadian Real Estate Association (CREA) is one of Canada’s largest single-industry associations. CREA works on behalf of more than 150,000 REALTORS® who contribute to the economic and social well-being of communities across Canada. Together they advocate for property owners, buyers and sellers.

For more information, please contact:

Pierre Leduc, Media Relations

The Canadian Real Estate Association

Tel: 613-237-7111 or 613-884-1460

E-mail: pleduc@crea.ca